President Trump once again has put America First, this time by promoting his so-called “Trump Accounts” — a new type of savings and investment account for children, created under the “One Big Beautiful Bill” Trump signed into law last year.

The program seeks to give every eligible American child a financial head start by providing a government-funded seed contribution and encouraging long-term saving and investing from birth.

Compare this to the government’s existing Head Start program, which is needlessly expensive, provides no educational benefits and in effect is a costly baby-sitting service.

Democrats favor policies that discourage investment, preferring that citizens become wards of the government, which of course they intend to control.

Americans save less of their income than most developed nations and consume more than they invest. Trump Accounts could help change this troubling trend.

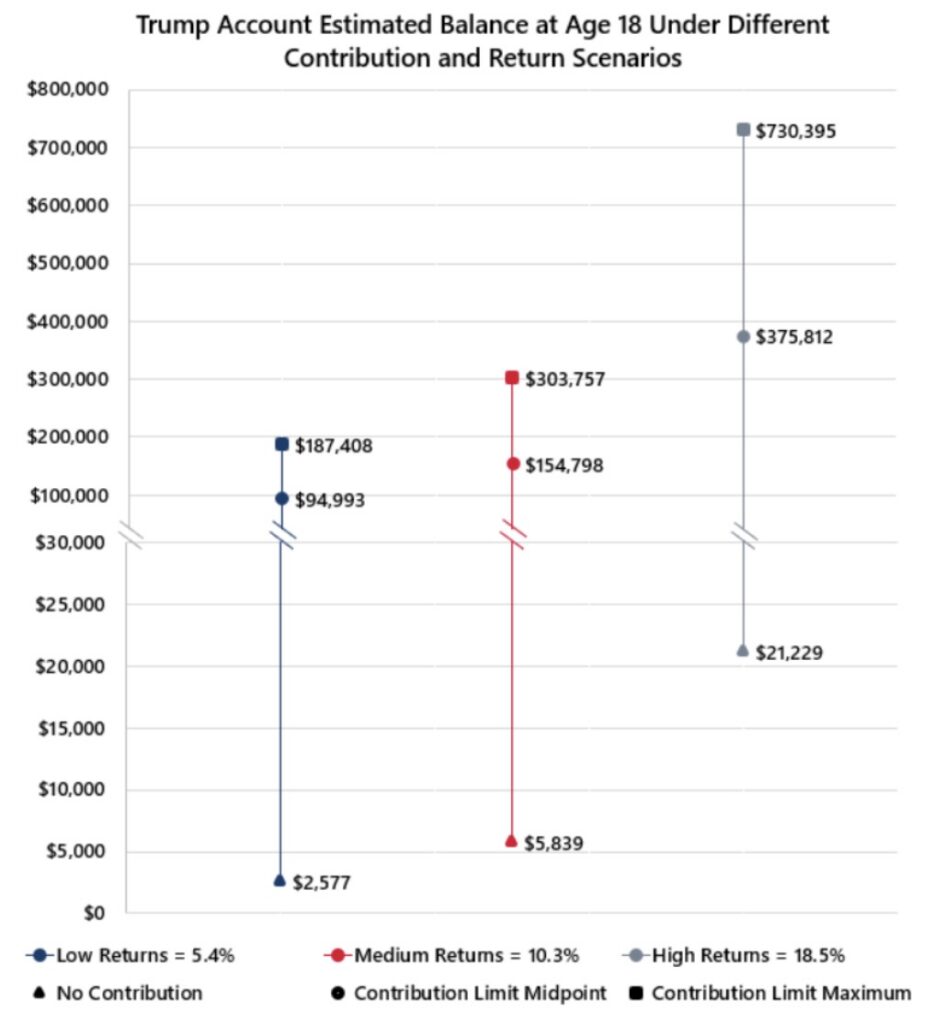

“We like the Trump Accounts because they are designed to create a nation of owners and it democratize stock ownership allowing today’s children to accumulate anywhere between $175,000 to $700,000 (depending how much supplemental money is put into the account) by the time they reach age 18,” economist Stephen Moore of the Committee to Unleash Prosperity said.

“By the time these kids reach 30, they could have as much as $1 million. We can be a nation of millionaires, and these accounts can and should replace most welfare programs in 20 years.”

The key features of Trump Accounts are:

- Eligibility: Any child born in the U.S. between Jan. 1, 2025, and Dec. 31, 2028, who is a U.S. citizen with a valid Social Security number, qualifies for a Trump Account.

- Government Contribution: The U.S. Treasury will deposit a one-time $1,000 into the account for each eligible child.

- Additional Contributions: Parents, employers, relatives, friends, local governments, and charities can contribute up to $5,000 per year. Contributions from governments and charities do not count toward the annual limit.

- Investment Rules: The funds must be invested in low-cost U.S. stock index funds (such as S&P 500), with annual fees capped at 0.10%. Private banks and brokerages manage the money.

- Withdrawal Rules: Money in the account is generally locked until the child turns 18. After that, it functions like a traditional IRA—funds can be withdrawn for education, a first home, or after age 59½ without penalties.

- Opening an Account: Parents can open Trump Accounts for eligible children using IRS Form 4547, either while filing taxes or through an online portal (available by summer).

Major financial institutions such as Bank of America, Wells Fargo, Charles Schwab, and others have pledged to match the $1,000 government contribution for their employees’ children, effectively doubling the initial balance for those families. Tech billionaires and celebrities also have pledged billions in supplemental contributions for eligible children.

Trump is a businessman, which is one of the reasons he got elected.

As such, he understands finance. He knows such a program can:

- Encourage early wealth-building and financial literacy.

- Help families save for major life expenses (education, home ownership, retirement).

- Expand private ownership and compound growth opportunities to all Americans.

Trump has worked tirelessly in his second term – free from phony impeachments and frivolous charges, although twice the target of assassins – sealing the borders, promoting election security, restoring respect for America worldwide and now trying to shift Americans from dependence to independence. It’s a record few could match.